We’re in the midst of a major economic transition, one that may eventually match the changes of the Industrial Revolution. The change, of course, is the advent of the green economy, and the switch from fossil fuel energy sources to renewable energy. While wind and solar power are soaking up the headlines, a more plausible long-term green power source is already near at hand: hydrogen.

Hydrogen, the most common element in the universe, is all around us – highly reactive and non-polluting. When used as a power source in chemical fuel cells, the chief byproduct is simple water. Hydrogen-fueled power systems have the potential to replace a host of combustion engine applications and vehicles.

We’re already witnessing this on a small scale in Canada, where a hydrogen train, manufactured by the French firm Alstom, is currently running a 3-month demo in Quebec. Carrying 120 passengers, the train matches the performance of conventional diesel engines. Once the Canadian demo wraps up in September, the plan is to tour other North American cities. Meanwhile, in Europe, such trains are already in service in 8 countries, including Germany, Italy, and France.

Unlike wind and solar power, which require extensive installation facilities, the US already produces 10 million metric tons of hydrogen annually, mainly for use in oil refining and ammonia production.

As a result, publicly traded companies in the US are already banking on hydrogen power and producing the fuel cell and electrolyzer technology needed for a nationwide hydrogen power network. According to TipRanks’ database, two of the industry leaders have garnered a ‘Buy’ rating from analysts, with a potential upside of over 50% for the upcoming year. Let’s take a closer look.

Plug Power (PLUG)

First up is Plug Power, a company working on hydrogen fuel cells that power the alternative energy economy. The company operates at an industrial and utility-grade scale at all stages of the process, from development to deployment. In addition to fuel cells, it also builds power storage systems and the necessary physical delivery infrastructure to bring fuel cell generation online at an industrial and utility-grade scale.

Like all hydrogen fuel cells, Plug’s systems generate electricity through electrochemical reactions based on hydrogen. The company can produce, liquefy, transport, and store fuel-grade hydrogen, deriving the fuel source from plain, clean water. The company’s fuel cell products have zero polluting emissions and have found applications as backup power generation and as battery power sources for industrial and warehousing machinery. The company counts major names, such as Amazon, Carrefour, and Walmart, among its customer base.

Plug boasts that it is the world leader in hydrogen fuel systems and use. To date, the company has deployed more than 60,000 fuel cell systems and built out a fueling network with more than 180 stations. Plug is the world’s largest buyer of liquefied hydrogen.

While the expansion of the hydrogen sector is fairly new, Plug has been able to leverage it for rising revenues over the last several years. As the company prepares to report its 2Q23 results on August 9, let’s take a look back at Q1 to get an idea of where it stands.

During Q1, Plug reported $210.3 million at the top line, showing an impressive 49% year-over-year growth and surpassing the forecast by $2.63 million. However, the bottom line was less rosy, with Plug’s earnings losses deepening. The company recorded a negative EPS of 35 cents, which was 9 cents deeper than anticipated. Moreover, Plug faced challenges with cash burn, utilizing $277 million compared to $210 million in the previous year’s quarter. In 1Q22, Plug had $3.1 billion in cash on hand, but by 1Q23, it decreased to $1.37 billion. Furthermore, Plug’s full-year revenue guidance for 2023 fell short of expectations, with projected figures ranging from $1.2 billion to $1.4 billion, compared to the forecast of $2.04 billion.

On the positive side, Plug has announced some recent deals that promise to expand its business globally. One of these, in Europe, is a secured order for 100 megawatts of PEM electrolyzers, and the second, in Australia, is an order for two 5-megawatt PEM electrolyzer units to be installed in the state of Tasmania.

The overall prospect for the hydrogen sector, and Plug’s built-in advantage as a leader in it, caught the eye of Northland analyst Abhishek Sinha, who writes, “We see PLUG’s momentum building up as its compounding opportunities are evolving in the hydrogen world. The company’s recent spate of project announcements in Europe is a testament to that… We feel that PLUG is now well positioned for a long run and barring any operational hiccups, should start generating FCF next year.”

Sinha follows up these comments with an Outperform (i.e. Buy) rating on the stock, and a $22 price target that suggests a 90% upside for the year ahead. (To watch Sinha’s track record, click here)

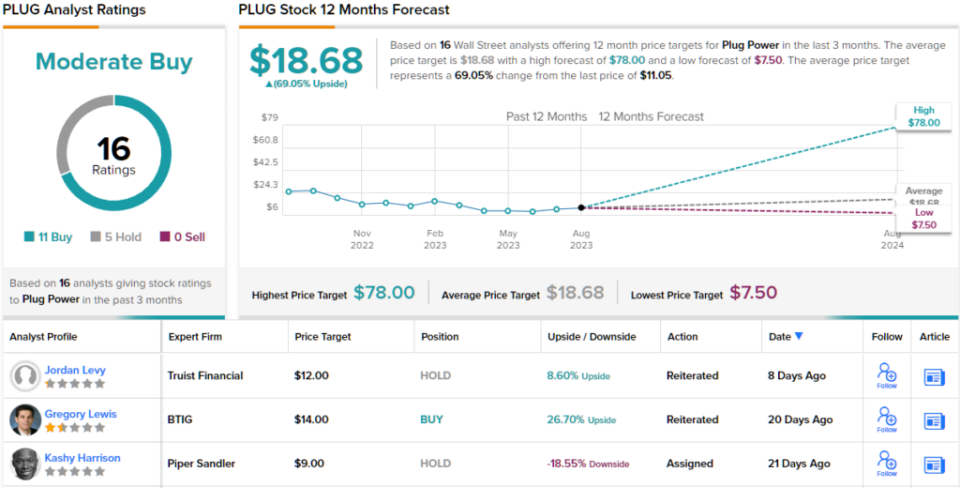

So, that’s Northland’s view, let’s turn our attention now to rest of the Street: PLUG’s 11 Buys and 5 Holds coalesce into a Moderate Buy rating. There’s plenty of upside – 69% to be exact – should the $18.68 average price target be met over the next months. (See PLUG stock forecast)

Bloom Energy (BE)

The second stock we’re looking at is Bloom Energy, another clean-energy company in the hydrogen fuel cell sector. Bloom is focused on electric power generation via solid oxide fuel cell technology, a clean power tech that uses a chemical reaction, specifically, the oxidation of a fuel, to produce usable electricity.

The cells offer solutions to issues of resiliency and sustainability that crop up in the clean energy sector; Bloom’s fuel cell tech is based on a proprietary solid oxide formulation that converts a variety of fuels, including natural gas, biogas, or simple hydrogen, into electrical energy without resorting to combustion. The result is a power source with ultra-low or zero carbon dioxide emissions, and with water or elemental hydrogen as the chief ‘exhaust.’

The company’s platform is called the Energy Saver. It is designed as an ‘always on’ system, able to provide power on demand whenever the customer wants or needs it. Bloom has designed the Energy Saver to be easily scalable, allowing installations to be fine-tuned to the customer’s needs and to be readily adaptable to expansion when required. The attraction of such a flexible energy source is clear, and Bloom has provided its power generation services to important companies such as Baker Hughes, the oil field services firm.

Bloom has also established long-term partnerships, working with various industrial firms to develop the potential of hydrogen fuel cells. One prominent partnership is with Korea’s Samsung Heavy Industries, in the marine shipping segment. Bloom is working with Samsung to develop ‘eco-friendly’ ships that will operate on electrical power generated through onboard fuel cells. Bloom is developing cells powered by liquid hydrogen and a polymer electrolyte, capable of meeting the power needs of a large oceangoing merchant vessel. This partnership dates back to 2019, and late last year, Samsung passed a milestone, receiving ‘approval in principal’ from the classification society DNV.

In Bloom’s last earnings report, for 2Q23, the company posted a top line of $301.1 million, up from $275 million in the previous quarter and representing a 23% gain year-over-year. On the negative side, the analysts had been looking for higher revenue; Bloom missed the forecast by $10.27 million.

Bloom’s non-GAAP EPS showed a similar pattern, improving year-over-year but missing the expectations. The company reported a loss of -$0.17 per share, an improvement compared to the earnings of -$0.20 in the previous year’s quarter. Nevertheless, analysts were anticipating a loss of -$0.14 per share.

In his coverage of Bloom for Raymond James, 5-star analyst Pavel Molchanov sees the company’s strongest suit as the flexibility of its products. Molchanov says of BE shares, “Bloom’s well-established positioning in fuel cells represents a play on climate adaptation, specifically the growing prevalence of grid outages. Entry into electrolyzers is a play on the nascent green hydrogen market, bolstered by European climate policy and the urgency of energy security, albeit the product rollout is taking longer than we had thought. The marine shipping collaboration with Samsung is an even earlier-stage opportunity.”

Looking ahead, Molchanov rates BE as an Outperform (i.e. Buy), and he sets a $25 price target to imply a potential upside of 59% in the next 12-months. (To watch Molchanov’s track record, click here)

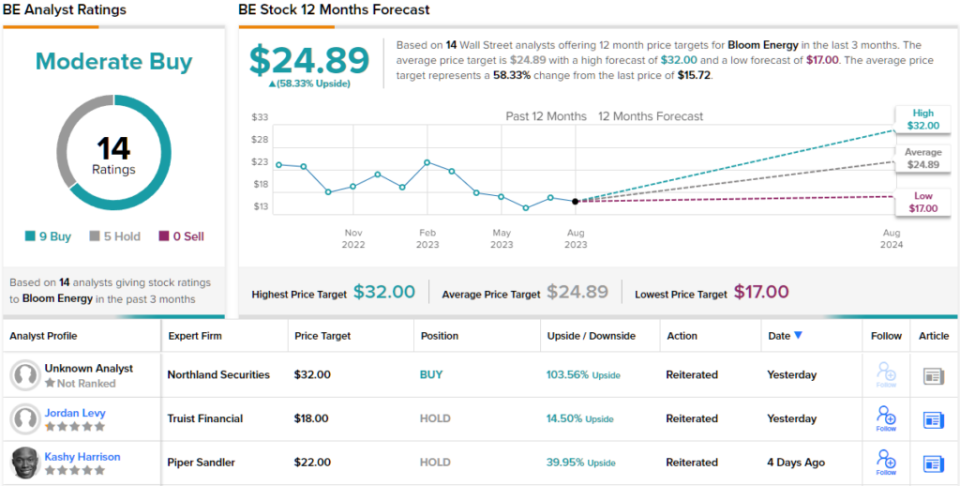

Overall, there are 14 recent analyst reviews on Bloom Energy, with a breakdown of 9 Buys against 5 Holds, for a Moderate Buy consensus. Bloom Energy shares have an average price target of $24.89, which suggests a 58% one-year upside from the current trading price of $15.72. (See BE stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.