Shares of the hydrogen fuel cell company Plug Power (NASDAQ:PLUG) have been kind of on the fritz lately, experiencing a decline of about 35% in August. The August 9 earnings report, which indicated Plug’s sales had risen by a robust 72%, also revealed losses that were 50% worse than what analysts had expected – a factor that contributed to the decline in the company’s stock.

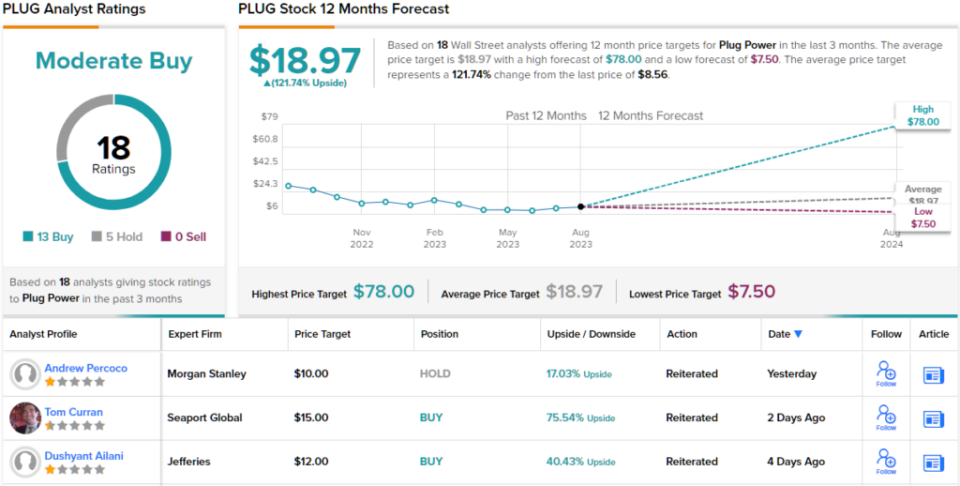

And yet, one analyst isn’t quite ready to throw in the towel on Plug just yet. In a recent note, Jefferies’ Dushyant Ailani took over coverage of Plug Power for the investment banker. And while Ailani trimmed Jefferies’ price target for Plug stock from $16 to just $12 a share, the analyst nonetheless maintained Jefferies’ “buy” rating on Plug.

Which kind of makes sense. After all, if Ailani believes the stock is worth $12 per share, it could still yield a potential profit of 40% from current levels, assuming the analyst is accurate about Plug stock’s value.

But is $12 the correct price?

Well, let’s consider: As Ailani reports, after 12 months of construction work, Plug is still in the process of getting its Georgian “green hydrogen” production process up and running. Already, this plant is producing gaseous hydrogen at the rate of three tons per day (tpd). But Plug needs to be producing liquid hydrogen to make the fuel source easily transportable and usable for fueling hydrogen fuel cell vehicles. Plug had hoped to be doing liquid hydrogen by the end of August, but that timeline has been pushed back a bit, to the end of the quarter — so September.

Plug hopes to ramp production volume as well, to about 15 tpd by the end of next month, or early October at latest. Then in phase 2 of the project, Plug hopes to double that production rate to 30 tpd by the second quarter of 2024.

So… good news, right? Well, not exactly. For one thing, Plug isn’t currently producing a whole lot of “green hydrogen” — i.e., hydrogen split from water molecules using power generated from renewable energy sources. Rather, the company is currently producing its hydrogen from “grey” sources — natural gas. And for another, Plug is still losing money at present, as noted above. In fact, even after the company begins producing liquid hydrogen and quintuples, its production capacity later this quarter, Ailani observes that gross “profit” margins for the company will probably still be negative 8%.

Translation: For every $1 of hydrogen Plug sells, the company will lose $0.08 — before adding losses from operating costs, interest on its near $1 billion in debt, and so on. On the bottom line, therefore, you can probably assume that Plug’s net profit margin is going to be a whole lot worse than just negative 8%. In fact, right now Plug’s net profit margin is negative 95%.

And yet, this fact doesn’t seem to faze Ailani, who is, after all, valuing Plug not on its profits (which Plug doesn’t have), but rather on Plug’s revenues (which it does). According to the analyst, a fair price to pay for Plug is about 4.5 times the $2.4 billion in sales the company may or may not make in 2025.

Overall, Wall Street has not given up on PLUG. The analysts have filed 18 analyst reviews in recent weeks, and these include 13 Buys against 5 Holds, for a Moderate Buy consensus rating. PLUG stock is priced at $8.54 and the $18.97 average price target suggests ~122% upside from that level. (See PLUG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.