Everyone likes a winner, and it’s only natural to gravitate toward them, but the stock market offers a unique twist on that process. That is because the biggest opportunities are often found among the losers, or more precisely, the stocks that have been beaten-down for one reason or another.

The interesting part is that in the stock market, these losers can quickly become winners, and those who were bold enough to pick up equities at depressed levels when they looked down and out will, in the end, reap the rewards.

But it’s not as simple as it sounds. Not all beaten-down stocks are destined to rebound; some might be languishing in the doldrums for a good reason. So, the key lies in identifying the stocks that are poised to bounce back eventually.

This is where Wall Street’s stock experts enter the frame. It is their job, after all, to point out where the best opportunities lie at any given time, and they will often tell investors to search for those equities that have been hit hard but deserve a second look.

With this in mind, we opened the TipRanks database to get the lowdown on 2 stocks that have received big haircuts this year – both are down by more than 50% – but for whom the analysts see much better days ahead. Each features a Strong Buy analyst consensus rating and offers triple-digit upside potential. Let’s take a deeper dive in.

Beam Global (BEEM)

We’ll start off with Beam Global, a clean-tech company specializing in innovative electric vehicle (EV) infrastructure solutions. The company is known for its solar-powered EV charging stations, which are designed to be both energy-efficient and versatile, catering to a wide range of applications, from public charging stations to fleet management and disaster relief efforts.

Notably, the company doesn’t compete directly with existing EV-charging companies; rather, it complements the services by supplying off-grid infrastructure solutions. Additionally, Beam maintains neutrality when it comes to EV-charging service equipment, meaning it doesn’t favor any specific EVSE (electric vehicle supply equipment) provider, allowing the company to cater to the broader industry.

A look at the growing revenue haul tells a compelling story. In Q2, revenue reached a record $17.82 million, amounting to a huge 379% year-over-year increase while beating the Street’s forecast by $3.8 million. The company generated a record Q2 gross profit of $0.5 million, representing a 3% gross profit margin. All told, at the bottom-line, EPS of-$0.32 was in-line with Street expectations.

Nevertheless, despite the strong growth, the stock is down by 55% year-to-date, and its decline can be partly attributed to the general difficulties faced by the EV charging space this year and the fact unprofitable growth stocks have fallen out of favor against a backdrop of rising interest rates.

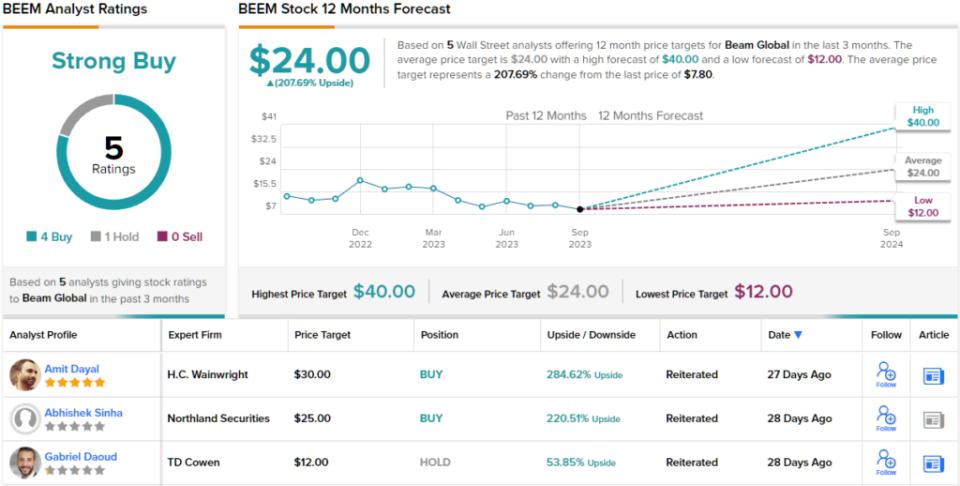

However, for Northland analyst Abhishek Sinha, BEEM’s improving fundamentals are the key point here.

“The company achieved yet another quarter of positive gross margin and expects that to further improve in 2H as favorable pricing, cost reductions and engineering efficiencies come into play,” Sinha said. “The company expects to close its Amiga acquisition in Q4 and leverage the lower cost structure of Serbia to further boost its margins. We believe BEEM offers a differentiated proposition in the public charging market space.”

Quantifying his stance, Sinha rates BEEM stock as Outperform (i.e., Buy) while his $25 price target implies shares will post growth of a robust 220% in the year ahead. (To watch Sinha’s track record, click here)

Overall, 3 other analysts join Sinha in the bull camp and with an additional 1 Hold, the stock claims a Strong Buy consensus rating. The $24 average target suggests the shares are set to triple in value over the next 12 months. (See BEEM stock forecast)

Avidity Biosciences (RNA)

For the next beaten-down stock, we’ll turn to the biotech sector and take a look at Avidity Biosciences. The company develops innovative RNA-targeted therapies to address different diseases. Avidity is known for its pioneering work in the field of antibody oligonucleotide conjugates (AOCs), a novel therapeutic platform that combines the precision of monoclonal antibodies with the specificity of oligonucleotide-based medicines.

The company’s focus right now is on developing AOCs for muscle disorders, and its lead candidate, AOC1001, is a TfR1-targeting monoclonal antibody conjugated to DMPK-targeting siRNA intended to treat Myotonic Dystrophy Type 1 (DM1).

In May, the FDA eased a partial clinical hold on AOC 1001, which was previously put in place after a subject in the 4 mg/kg cohort of the Phase 1/2 MARINA study developed a rare serious adverse event. The company is currently dose-escalating roughly 12 participants from 2 mg/kg to 4 mg/kg of AOC 1001 in the MARINA-OLE study. At the same time, details are being finalized for the design of a Phase 3 study and the global path ahead for the drug. An initial data readout from the MARINA-OLE trial is earmarked for 1H24.

Elsewhere in the pipeline, the FDA recently granted Orphan Drug designation for its investigational RNA therapeutic AOC 1044, intended to treat Duchenne muscular dystrophy (DMD) patients with mutations amenable to exon 44 skipping (DMD44). The Phase 1/2 study of AOC 1044 (EXPLORE44) is currently underway for patients living with DMD44. A data readout from EXPLORE44’s healthy volunteers is anticipated in Q4.

While investors have appeared skeptical about the stock following the adverse event – the shares are down 70% so far this year – Raymond James Steven Seedhouse’s positive thesis is based on the company overcoming the issue and the aforementioned drugs gaining a market entry eventually.

“Ultimately,” says the analyst, “we expect functional data will be important, and we expect Avidity to remove the partial hold and thus safety overhang at 4 mg/kg, run a pivotal study with vHOT or multiple functional endpoints as primary endpoint(s), and expect both therapeutics will ultimately be approved for and compete in DM1 market, which is a large multi-$B market.”

These comments underpin Seedhouse’s Strong Buy rating and are backed by a $71 price target. That figure factors in huge growth of 980% in the year ahead. (To watch Seedhouse’s track record, click here)

While that target might seem improbable, the rest of the Street’s take is hardly less bullish. RNA’s Strong Buy consensus rating is not only based on a unanimous 6 Buys, but the $37 average target makes room for one-year returns of 463%. (See RNA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.